Coffee prices rise in July after three months of decline

In July 2020, the ICO composite indicator increased by 4.7% to an average of 103.66 US cents/lb,

following three months of declines. Prices for all coffee groups rose in July 2020, though the largest

month-on-month increase occurred for Brazilian Naturals, which grew by 5.8% to 97.96 US cents/lb.

Global exports in June 2020 amounted to 10.57 million bags, 5.3% lower than June 2019 while

shipments in the first nine months of coffee year 2019/20 reached 95.36 million bags, 5.1% lower than

the same period last year. The majority of coffee continues to be exported as green coffee, accounting

for 90.4% of total coffee shipped between October 2019 and June 2020. Soluble coffee shipments

accounted for 9.1%, of the total, an increase of 1 percentage point from one year ago, while roasted

coffee shipments represented just 0.5%. A 2.9% decrease in global production to 168.01 million bags

has contributed to the lower volume of shipments.

After falling in each of the last three months, the monthly average of the ICO composite indicator

rose by 4.7% to 103.66 US cents/lb in July 2020. The daily composite indicator reached a low of

98.59 US cents/lb on 10 July before climbing to 114.25 US cents/lb on the last day of the month.

Strengthening of the Brazilian Real in the second half of the month supported prices in July as

well as concerns over temporary tightness in supply

Prices for all group indicators rose in July 2020. The largest increase occurred in the average

price for Brazilian Naturals, which grew by 5.8% to 97.96 US cents/lb. Colombian Milds increased

by 4.2% to 153.38 US cents/lb while Other Milds rose by 3.7% to 146.78 US cents/lb. As a result,

the differential between Colombia Milds and Other Milds increased by 17% to an average of

6.60 US cents/lb. The monthly average Robusta price increased by 4.8% to 67.69 US cents/lb.

The average arbitrage in July, as measured on the New York and London futures markets, rose by

7.9% to 48.28 US cents/lb. Additionally, volatility of the ICO composite indicator price increased

by 1.5 percentage points to 7.6%. The volatility for Colombian Milds and Other Milds both

increased by 1.1 percentage points to 6.7% and 6.9%, respectively. Brazilian Naturals volatility

rose by 2.8 percentage points to 11.5%, while the volatility for Robustas decreased by

0.3 percentage point to 6.3%.

Global coffee production in coffee year 2019/20 is estimated at 168.01 million bags, a decrease

of 2.9% from 2018/19. Arabica output is estimated to fall by 5.4% to 95.37 million bags, due to

a decline in production in seven of the ten largest Arabica producers, while Robusta production

is estimated to increase by 0.5% to 72.63 million bags. Global coffee consumption is estimated

to rise by 0.3% to 168.49 million bags, which is below the average annual growth rate of 2.2%

over the last two decades. Strong growth at the start of the season is expected to be offset by a

global economic slowdown.

In June 2020, world coffee exports fell by 5.3% to 10.57 million bags compared to June 2019,

due in part to lower production. Shipments of Arabica fell by 10% to 6.42 million bags, but

Robusta exports increased by 3% to 4.15 million bags compared to June 2019. Global exports in

the first nine months of coffee year 2019/20 decreased by 5.1% to 95.36 million bags. Shipments

of Other Milds shrank by 8.2% to 19.11 million bags in October 2019 to June 2020. Brazilian

Naturals decreased by 7.8% to 28.84 million bags while Colombian Milds exports fell by 7.2% to

10.53 million bags in the first nine months of the coffee year. Robusta shipments reached

36.88 million bags, 0.4% lower than in October 2018 to July 2019.

In the first nine months of coffee year 2019/20, green coffee exports represented 90.4% of total

exports, amounting to 86.2 million bags. This current trend is only slightly lower than that

observed three decades ago, when green exports accounted for around 95% of total exports,

indicating that much of the value addition remains in importing countries. Soluble coffee

shipments accounted for 9.1%, of the total, an increase of 1 percentage point from one year ago,

while roasted coffee shipments represented just 0.5%. Total exports of soluble coffee reached

8.64 million bags and roasted coffee exports reached 509,000 bags in the first nine months of

coffee year 2019/20.

In October 2019 to June 2020, Brazil shipped 26.48 million bags of green coffee, 9.5% lower

than the same period one year ago, and accounted for around 30.7% of all green coffee

shipments. Green coffee exports from Viet Nam reached 20.22 million bags in the first nine

months of coffee year 2019/20, representing 23.5% of the total and making it the second largest

exporter of green coffee. Colombia’s green coffee exports fell by 7.4% to 8.72 million bags and

shipments from Honduras declined by 14.1% to 4.81 million bags. However, green exports from

both Uganda and Indonesia rose, increasing by 20.6% to 3.79 million bags and by 30.2% to

3.37 million bags, respectively. The main destinations for green coffee were the United States,

Germany, Italy, Belgium, and Japan in October 2018 to July 2019.

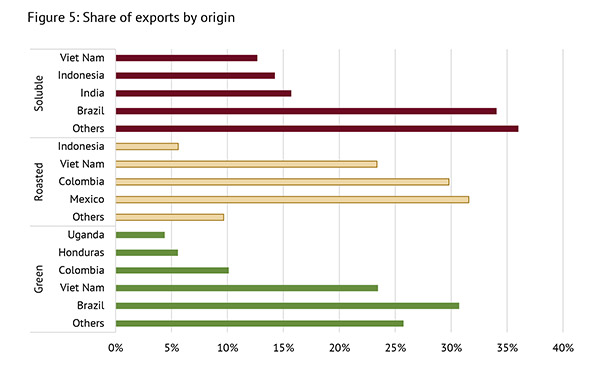

Mexico, Colombia, Viet Nam, Indonesia, and Brazil represent the five largest exporters of roasted

coffee among coffee producing countries, accounting for 93.1% of total roasted coffee exports in

the first nine months of coffee year 2019/20. Mexico shipped 161,000 bags of roasted coffee

while Colombia exported 152,000 bags. Viet Nam’s exports of roasted coffee declined by 52.3%

to 119,000 bags, and Brazil’s shipments of roasted coffee by 25.4% to 14,200 bags. However,

Indonesia’s exports of roasted coffee more than tripled to 28,600 bags. The United States was

the main destination for shipments of roasted coffee, accounting for around 45.7% of the total

during the first nine months of 2019/20.

Brazil was the largest exporter of soluble coffee in October 2019 to June 2020, with shipments

reaching 2.94 million bags, 1.8% lower than the same period one year ago. India exported

1.36 million bags, 5.3% lower than the first nine months of coffee year 2018/19. Soluble exports

from Indonesia rose by 47.3% to 1.23 million bags and Viet Nam’s soluble shipments grew by 11% to 1.09 million bags. Mexico’s soluble exports rose by 11.8% to 670,00 bags and Colombia’s

exports by 2.4% to 630,000 bags. These six countries accounted for 91.7% of total soluble

shipments in the first nine months of coffee year 2019/20. The United States, the Philippines,

the Russian Federation, Poland and Malaysia were the main destinations for soluble shipments

in October 2019 to June 2020.

Explanatory Note for Table 3

For each year, the Secretariat uses statistics received from Members to provide estimates

and forecasts for annual production, consumption, trade and stocks. As noted in paragraph

100 of document ICC 120-16, these statistics can be supplemented and complemented by

data from other sources when information received from Members is incomplete, delayed or

inconsistent. The Secretariat also considers multiple sources for generating supply and

demand balance sheets for non-Members.

The Secretariat uses the concept of the marketing year, that is the coffee year commencing

on 1 October of each year, when looking at the global supply and demand balance. Coffee producing countries are located in different regions around the world, with various crop

years, i.e. the 12-month period from one harvest to the next. The crop years currently used

by the Secretariat commence on 1 April, 1 July and 1 October. To maintain consistency, the

Secretariat converts production data from a crop year basis to a marketing year basis

depending on the harvest months for each country. Using a coffee year basis for the global

coffee supply and demand, as well as prices ensures that analysis of the market situation

occurs within the same time period.

For example, the 2014/15 coffee year began on 1 October 2014 and ended 30 September

2015. However, for producers with crop years commencing on 1 April, the crop year

production occurs across two coffee years. Brazil’s 2014/15 crop year began on 1 April 2014

and finished 31 March 2015, covering the first half of coffee year 2014/15. However, Brazil’s

2015/16 crop year commenced 1 April 2015 and ended 31 March 2016, covering the latter

half of coffee year 2014/15. In order to bring the crop year production into a single coffee

year, the Secretariat would allocate a portion of the April-March 2014/15 crop year

production and a portion of the April-March 2015/16 production into 2014/15 coffee year

production.

It should be noted that while estimates for coffee year production are created for each

individual country, these are made for the purpose of creating a consistent aggregated

supply-demand balance for analytical purposes, and does not represent the production

occurring on the ground within the individual countries